Business for wood components manufacturers, particularly those involved in the residential segment, continues to be fairly steady as North America emerges from the coronavirus pandemic.

A recent survey of more than 150 component and dimension producers found that although they were initially hard hit by the COVID 19 pandemic, as evidenced by the 61.9% that reported negative effects in the first half of 2020, by the second half of 2020 that had lessened to 33.1%. Interestingly, 56.1% saw a positive effect on their business, likely due in part to the upswing in renovations as homeowners sheltered in place. And when asked for their 2021 sales projections, practically all, 86.4%, are optimistic.

Sales and business performance information was compiled in the fourth annual Wood Components Benchmark Study, conducted in late February through early May by the Wood Products Manufacturers Association, the Wood Component Manufacturers Association and Woodworking Network. What follows is a snapshot of the industry based on the survey results.

Where is the business?

Before, during, and it after the pandemic, residential applications outweigh commercial. When asked what industries they sell to, 84.6% of respondents sell to the residential cabinetry and closets market, with the segment accounting for all or three-quarters of sales for 25.3%. Likewise, 69.0% of the respondents sell at least some product to the residential furniture market, with 14.3% selling to it almost exclusively. In comparison, 71.3% of respondents sold product into the commercial cabinetry market, 11.5% almost exclusively, while 65.5% were involved in contract furniture, including 4.8% for whom the segment provided 75% or more of their sales.

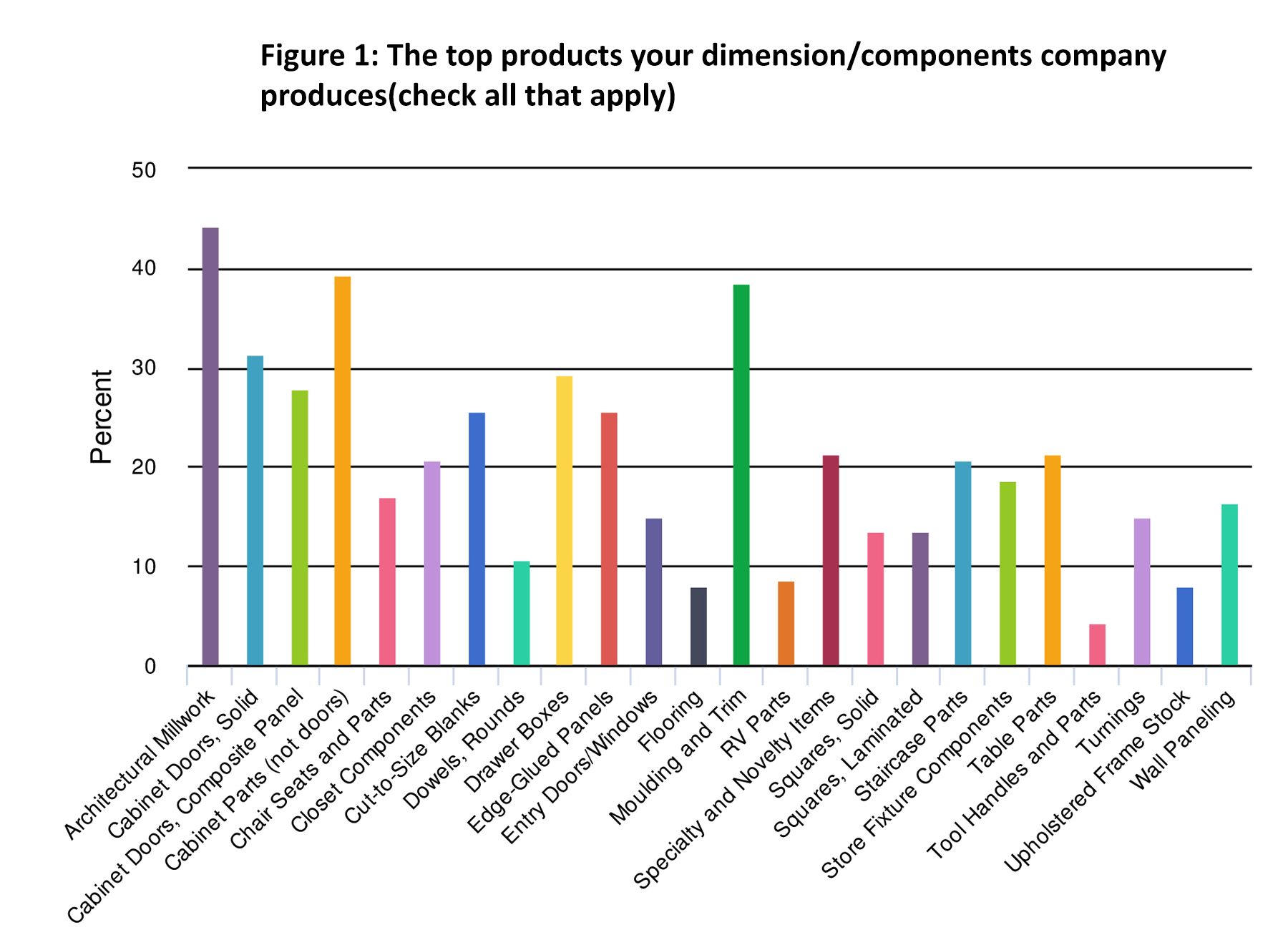

Of the remaining markets, 72.2% had sales in building products, 72.7% decorative/specialty and 53.8% provided some level of industrial products. A drill-down of some of the product offerings and how they rank is shown in Figure 1.

Not surprisingly, the combined cabinetry components category (cabinet parts, cabinet doors, and drawer boxes) accounts for the largest product segment, followed by architectural millwork and moulding and trim.

When asked if they exported their products, 82.1% responded no; of those that do export, 68.0% said the sales generated accounted for just 1-25% of their overall total, 8.0% said 26-50%, 12.0% cited 51-75% and 12.0% said 76-100%.

With regards to the species used by producers of these products, respondents ranked hard maple at the top, followed by red oak, poplar, white oak and soft maple, although this could change as lumber shortage issues continue.

The popularity of laminated components, including those utilizing thermally fused laminate (TFL), 3D laminates (3DL), 2D laminates (2DL), high-pressure laminate, as well as decorative foils and papers, had 33.8% selecting composite panel (MDF/particleboard) from the list, with 33.8% also listing plywood. (Figure 2.)

Business plans

Not surprisingly, 86.4% of the respondents projected 2021 net income to be the same or higher, of that number, 48.8% said somewhat higher and 17.6% projected much higher.

Almost all survey respondents also expect to see increases in expenditures, particularly in raw materials, with 92.7% predicting higher costs, and of those, 57.7% projecting “much higher” costs.

Plant and equipment expenditures are projected to remain steady by 44.6% of respondents, with another 47.9% planning expenditures. And with the labor market a top concern, 63.3% of survey respondents foresee employee costs rising in 2021, while 33.3% expect them to remain steady.

The fourth annual Wood Components Benchmark Study provides insight into market sales, product categories, and business performance projections and other relevant information. Respondents came from the Northeast United States (22.5%), Southeast (14.1%), Midwest (33.8%), Western United States (10.6%), Quebec (3.5%), Ontario (6.3%), British Columbia (2.1%) and Alberta (1.4%) and other (5.6%) which includes Manitoba and Mexico.

For more information about the study or the sponsoring organizations, contact the Wood Products Manufacturers Association at 978-874-5445, [email protected] or by visiting WPMA.org; the Wood Component Manufacturers Association at 651-332-6332, [email protected] or by visiting WCMA.com. View related articles on Woodworking Network at woodworkingnetwork.com.

Have something to say? Share your thoughts with us in the comments below.